The Price of Profits

In a few of my recent notes, I’ve discussed how to think about a company’s market value.

Capital forms the foundation of that value. A company builds upon that foundation with competitive profits .

So far, I’ve used Oracle Corp. (NASDAQ: ORCL) as an example. And I’ll stick to it since Oracle is the topic of my next Capital InFocus report.

As a refresher, Oracle’s capital based on the most recent financials equals $99.9 billion, with Goodwill, through acquisitions, contributing the most to that capital.

Its competitive profits over the last 12 months equal $6.06 billion.

Today, we’ll take a look at how much those profits are worth relative to Oracle’s current $168 stock price.

But first, we’ll use that stock price to understand what value the market has placed on Oracle’s business.

What the Market Thinks

You can tell how much the market considers a company’s enterprise to be worth by adding the value of its equity (i.e., stock) and debt.

We call this total the Market Value of a company and equals the sum of its Common Stock Market Capitalization and Debt (which include the present value of rents).

You get the market cap by multiplying the company’s stock price by the total number of shares outstanding. At Oracle’s current $168 share price, its market cap equals $465.8 billion.

The value of its debt and rent is $85.4 billion.

Adding those together and after a couple of adjustments (not worth diving into here), you get a total market value for Oracle of $551 billion.

That’s the value the market places on Oracle.

Assuming you could get your hands on $551 billion, you could buy Oracle’s outstanding debt and stock and own the company outright.

Now, we’ll approach that market value from the other side to see how much that market value depends on future competitive profits. That way, you will know just how much you’re betting on the future when paying $168 for Oracle’s stock.

Depending on Future Profits

A company is worth what you would pay for its capital plus what you would pay for its future competitive profits.

Capital is only worth the minimum it needs to return in a competitive market.

This minimum return is the Cost to Compete that I discussed in Don’t Fall for Lazy Profits.

What this means for you as an investor is that, when a company isn’t expected to earn competitive profits, it is only worth the value of its capital (or less).

However, when a company’s market value exceeds the value of its capital, it must be because the market expects that company to generate competitive profits in the future.

With Oracle’s $551 billion market value in hand and $99.9 billion in capital, you can parse out how much of its market value depends on future competitive profits.

I call the difference between market value and capital the company’s Market Value Add, which is labeled MVA below. It’s how much value the market adds to Oracle’s capital based on its current stock price.

That additional value depends 100% on future competitive profits.

Remember: A company is worth its capital plus the value of future competitive profits.

For Oracle, $451.1 billion of that $551 billion market value hangs on what it can deliver in the future.

If Oracle fails to deliver, then the stock price will fall. If you think the company will do better than that, then it could be time to buy the stock.

In either case, Market Value Add tells you what the market thinks Oracle’s future competitive profits are worth.

But I don’t stop there.

The Future in Two Parts

We can break the future into two parts. One part that reflects the value of profits that stay the same. And a second that reflects the value of profits either growing or declining.

I call the value of unchanged future profits Current Value Add (or CVA). The amount that future profits grow (or fall) is called Future Value Add (or FVA).

It’s like this: MVA = CVA + FVA

We figured out earlier that the market values Oracle’s future profits at $451.1 billion.

We also know that Oracle’s competitive profits over the last twelve months equals $6.06 billion. The value of those profits projected into the future, its CVA, is worth $82.9 billion today (trust me on that one, we’ve covered enough ground today).

So, plugging what we know into the above formula: $451.1 billion = $82.9 billion + FVA

Alakadabra, do some simple algebra, and you will see that the market values future profits at $368.2 billion.

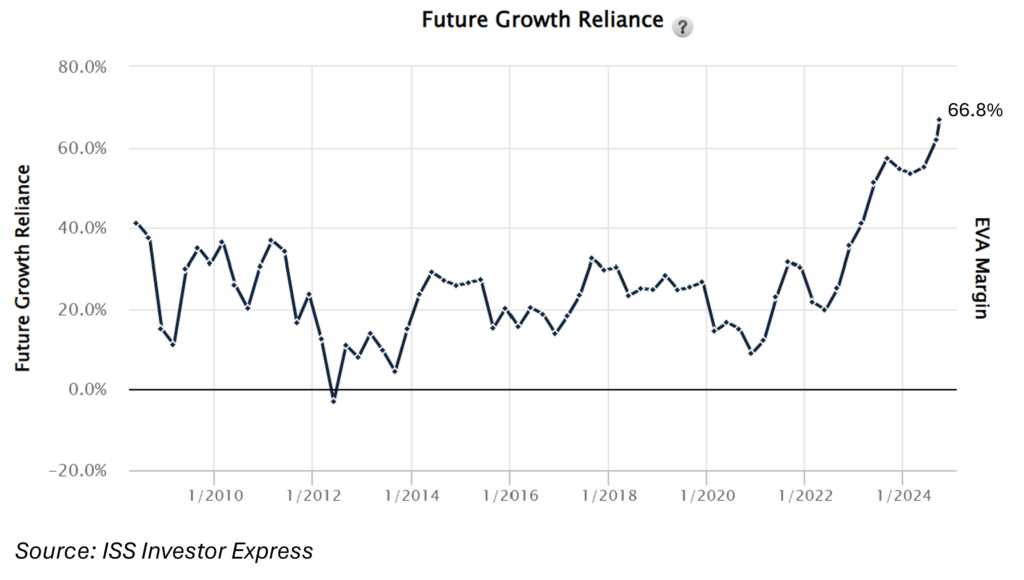

You can see my breakdown of the value of future profits here:

Breaking the future into unchanged profits and growth lets you see how much a company’s market value relies on future growth.

The FVA is the premium (or discount when negative) priced into the company’s stock.

To see how this premium compares across companies, sectors, indexes, or time, divide that $368.2 billion premium by its total $551 billion market value.

Here’s how that premium compares to Oracle’s history.

This measure is called Future Growth Reliance, and it tells us that 66.8% of Oracle’s market value relies on future growth.

That’s what’s baked into the cake. And, relative to Oracle’s history, the stock seems rich.

But you need more than one statistic to answer whether Oracle is worth the price.

When you buy the stock, you own the value of future profits, no matter what they turn out to be.

The question now is whether profits could be greater or less than what the markets have priced in.

Is $168 too expensive, or is it a bargain?

I answer that question in my Capital InFocus report on Oracle.

Until then…

Think Free. Be Free.

Don Yocham, CFA

Managing Editor of The Capital List

Related ARTICLES:

American Exceptionalism, v2.0

By dustin

Posted: February 12, 2025

The years following WWII brought America into an era of exceptionalism. We emerged as the war’s only true victor. Fighting the war necessitated a...

The Holy Trinity of Growth

By dustin

Posted: February 7, 2025

The War for the American Way has begun. Since taking office on January 20, Trump and his administration have launched a full-scale assault against...

The War for the American Way

By dustin

Posted: February 7, 2025

Since his ascension to office on January 20, Trump and Co. have launched a full-scale assault on the vast, unaccountable bureaucracy draining the U.S....

Draining the Moat

By dustin

Posted: February 2, 2025

DeepSeek threw a monkey wrench into a powerful AI narrative last week. It challenged the story that developing AI models requires capital that only...

Deep-Sixed AI Dreams

By dustin

Posted: January 28, 2025

Let’s play Never Have I Ever. I’ll go first. Never have I ever seen a market narrative crushed so thoroughly over a weekend. Until...

From FUD to Oil and Gas Clarity

By dustin

Posted: January 25, 2025

For the past four years, traditional energy stocks received no love from investors. Green energy initiatives hamstrung oil and gas stocks with fear, uncertainty,...

Waking Up to the “Drill Baby, Drill” Dream

By dustin

Posted: January 22, 2025

I first pointed out the opportunity emerging in traditional energy companies in August. As the Magnificent Seven lit up the charts with AI potentiality,...

This Ain’t Your Mother’s Internet Bubble

By dustin

Posted: January 21, 2025

Just a short note for you today as we head into the long weekend. You hear a lot about how the AI bubble is...

Tariff Winners and Losers

By dustin

Posted: January 17, 2025

T-minus 4 days until the terror becomes real in D.C. Inauguration Day will be upon us, and the D.O.G.E. becomes manifest for the parasite...

The Odds Favor Growth

By dustin

Posted: January 14, 2025

Capital markets don’t hide their expectations for the future; they hold them out for all the world to see. Assuming you know where to...

FREE Newsletters:

"*" indicates required fields