Hope With a Heaping Side of Caution

So, I missed the clown show, ahem… debates on Tuesday night.

It was deliberate.

They provide as much information as Inside Edition or TMZ.

That’s not how I prefer to waste my time.

I know that plenty of thinking people on the fence watched in hopes of learning something useful. Not everyone blindly accepts party-dictated talking points or social media memes.

From what I saw of the debates on replay and chatting with a few independent-minded friends, however, they surely walked away disappointed.

You gotta give some credit to Kamala’s handlers, though. Telling “The Apprentice” star “you’re fired” was both obvious and brilliant.

They clearly worked shopped his trigger words.

It paid off.

As a buddy at my gym said, “Kamala shook him up like a bottle of coke.”

The debates may have failed to inform voters. But at least we gained a new definition of pet food.

With so little learned and so few opinions swayed, it’s still a coin toss as to what kind of country we will wake up to on November 6th.

But no matter who wins, the playbook for markets remains the same.

CapEx Driven Growth

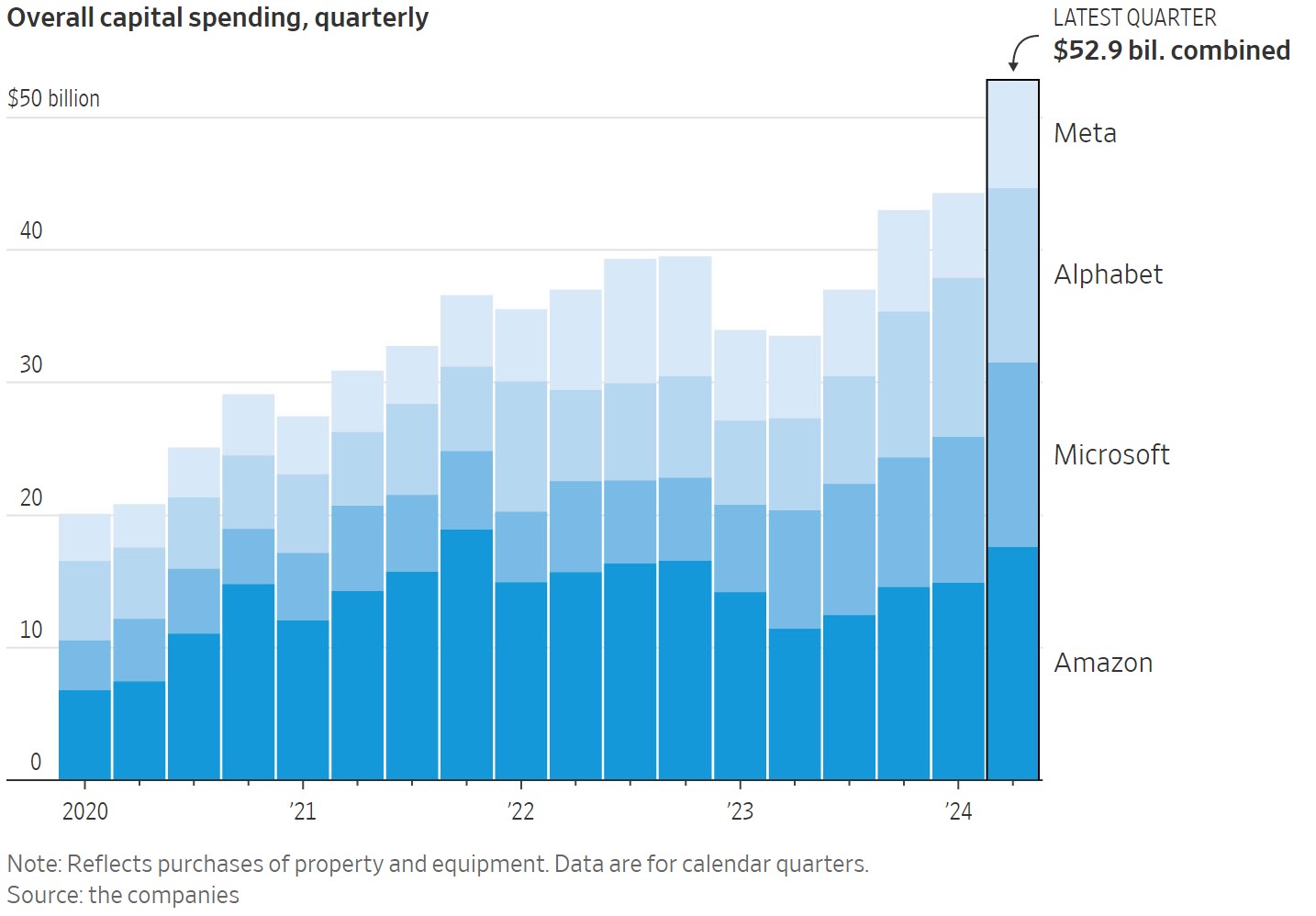

Capital spending by tech companies to take the lead in the AI race has only begun.

As pointed out in Tuesday’s Wall Street Journal, Amazon, Microsoft, Alphabet (Google), and Meta spent a combined $52.9 in the latest quarter.

Oracle also proved itself an AI contender with a 45% jump in its Oracle Cloud Infrastructure business segment.

As Oracle co-founder Larry Ellison said during the earnings call, “If your horizon is over the next five years, maybe even the next ten years, I wouldn’t worry about it,” and went on to say “This business is just growing larger and larger and larger. There is no slowdown or shift coming.”

His statement echoed the sentiment of Google’s CEO, who said earlier this summer, “The risk of underinvesting is dramatically greater than the risk of overinvesting for us here.”

Microsoft has doubled its data center footprint in the last four years. Google expanded by 80%.

And Oracle plans to build 100 new data centers over the coming years.

The hundreds of billions in data center capex coming down the pike pulls along a massive amount of other investment with it in the form of cooling systems, networking equipment, and power plants. It flows through the economy and lays the foundation for economic growth the right way.

Will it pay off in terms of earnings?

That depends.

Revenue Now vs Revenue Later

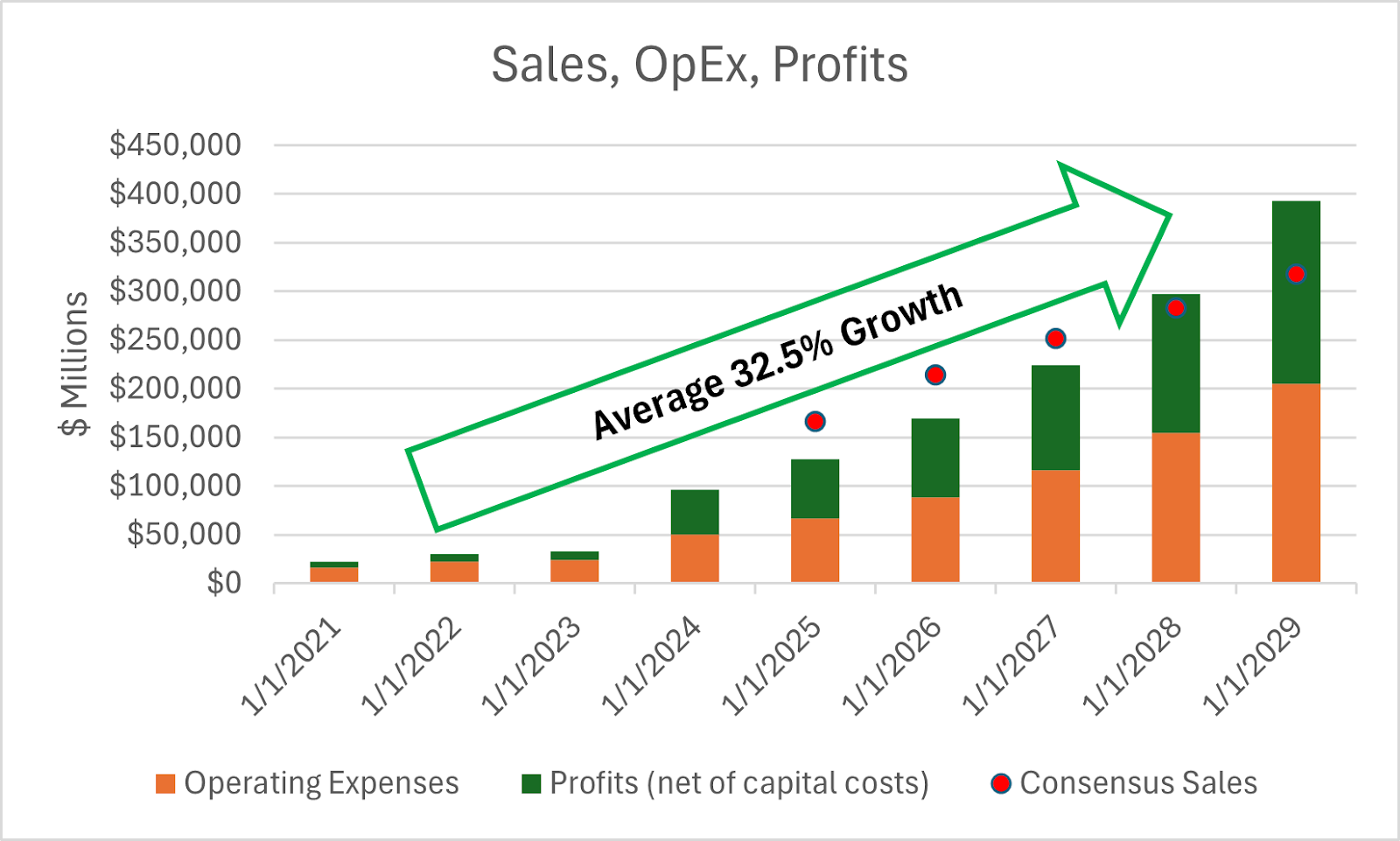

For Nvidia, yes. All this capex spending by big tech means revenue for Nvidia.

Over the next 5 years, Nvidia’s revenue must grow at an average of 32.5% per year to justify its current $118 share price, taking sales from $96.3 billion to $393 billion.

Source: ISS Investors Express, The Capital List

That’s only slightly more than consensus estimates and achievable given its 194% revenue growth over the past year.

But we don’t have to wait 5 years to justify today’s price. Should Nvidia continue to trounce estimates over the next couple of quarters, that “justified price” will climb higher, and its actual price will quickly follow.

To see why Nvidia is worth the price, check out my latest research on the company here.

For other companies like Microsoft, Google, Amazon, and Meta doing the investing, however, the AI payoff could still be years in the future.

So take care. With market players focusing more on the payoff than they did six months ago, big stock market gains may be harder to come by.

Now is not the time to get aggressive, especially with a recession on its way.

Low Value, Low Growth

And it’s not just the economy that could send stocks lower.

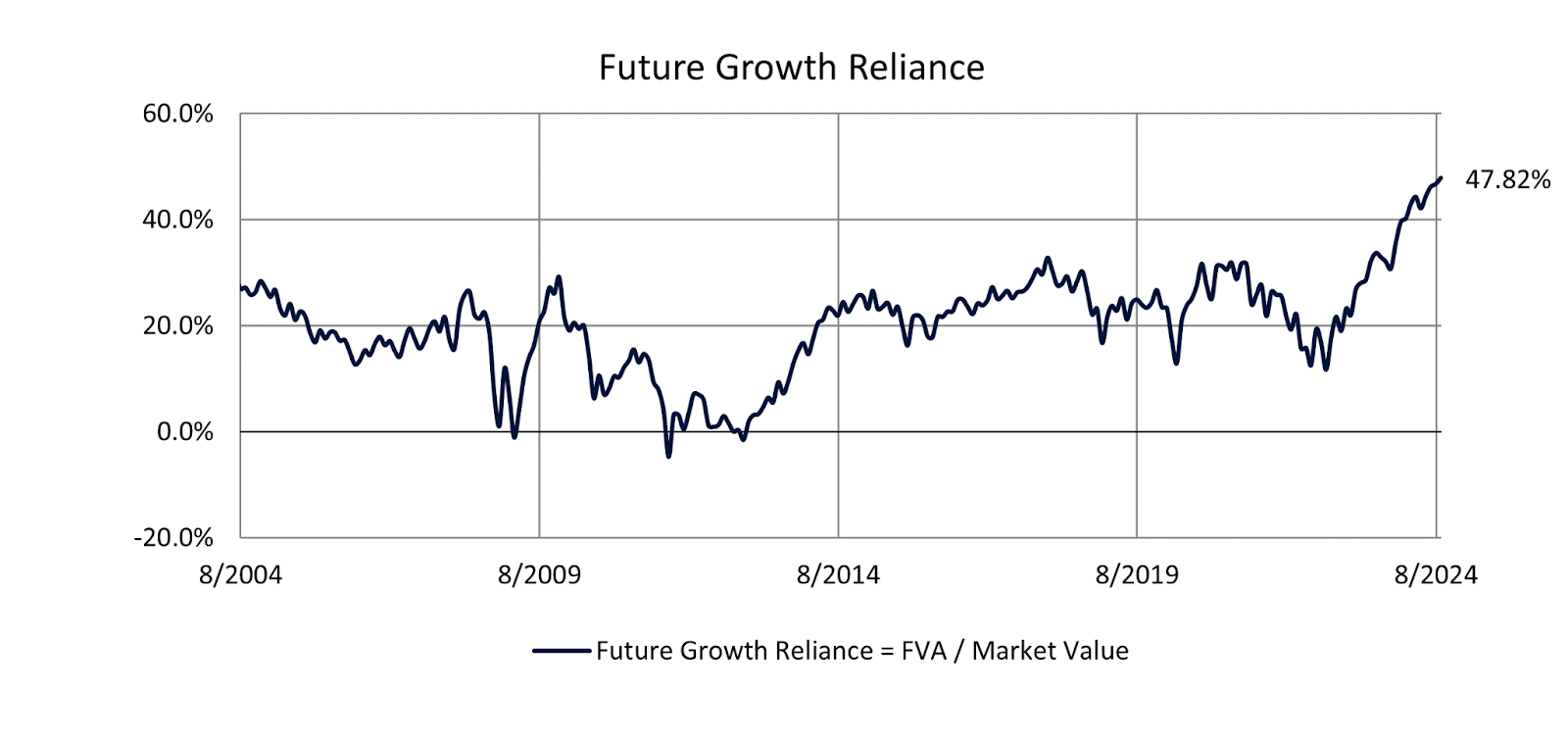

The S&P 500 rallied 59% over the past two years. So, unsurprisingly, valuations are stretched. Nearly 48% of the S&P’s current 5,568 price depends on future profit growth—a level not seen in the past 20 years.

Source: ISS Investors Express, The Capital List

To this list of concerns, you also need to add in global growth headwinds.

The ECB just cut rates to avert a slowdown while still not having solved inflation.

China’s economy continues to struggle, and it will only get worse as they try to export state-subsidized overproduction to buy their way out.

And, no matter whose clown wins the election, trade wars are here to stay. That’s not only bad for growth but bad for inflation too.

Plus, trade wars easily lead to hot wars.

Then, there’s the potential for a crisis among regional banks as CRE loans go bust. Which the Fed could be trying to get ahead of with rate cuts that seem hard to justify as well.

The market could continue higher for sure. Apart from tepid sentiment, I see no other catalyst to kick stocks lower in the near term.

But you’ll end up further ahead by leaving some dry powder in your accounts than if you keep piling in at the top.

Think Free. Be Free.

Don Yocham, CFA

Managing Editor of The Capital List

Related ARTICLES:

American Exceptionalism, v2.0

By Don Yocham

Posted: February 12, 2025

The years following WWII brought America into an era of exceptionalism. We emerged as the war’s only true victor. Fighting the war necessitated a...

The Holy Trinity of Growth

By Don Yocham

Posted: February 7, 2025

The War for the American Way has begun. Since taking office on January 20, Trump and his administration have launched a full-scale assault against...

The War for the American Way

By Don Yocham

Posted: February 7, 2025

Since his ascension to office on January 20, Trump and Co. have launched a full-scale assault on the vast, unaccountable bureaucracy draining the U.S....

Draining the Moat

By Don Yocham

Posted: February 2, 2025

DeepSeek threw a monkey wrench into a powerful AI narrative last week. It challenged the story that developing AI models requires capital that only...

Deep-Sixed AI Dreams

By Don Yocham

Posted: January 28, 2025

Let’s play Never Have I Ever. I’ll go first. Never have I ever seen a market narrative crushed so thoroughly over a weekend. Until...

From FUD to Oil and Gas Clarity

By Don Yocham

Posted: January 25, 2025

For the past four years, traditional energy stocks received no love from investors. Green energy initiatives hamstrung oil and gas stocks with fear, uncertainty,...

Waking Up to the “Drill Baby, Drill” Dream

By Don Yocham

Posted: January 22, 2025

I first pointed out the opportunity emerging in traditional energy companies in August. As the Magnificent Seven lit up the charts with AI potentiality,...

This Ain’t Your Mother’s Internet Bubble

By Don Yocham

Posted: January 21, 2025

Just a short note for you today as we head into the long weekend. You hear a lot about how the AI bubble is...

Tariff Winners and Losers

By Don Yocham

Posted: January 17, 2025

T-minus 4 days until the terror becomes real in D.C. Inauguration Day will be upon us, and the D.O.G.E. becomes manifest for the parasite...

The Odds Favor Growth

By Don Yocham

Posted: January 14, 2025

Capital markets don’t hide their expectations for the future; they hold them out for all the world to see. Assuming you know where to...

FREE Newsletters:

"*" indicates required fields