Flawed Motive Behind the Fed’s Rate Cut Agenda

For every thing, there is a season.

According to Jerome Powell, the season calls for cuts.

At the annual Jackson Hole confab held by the Federal Reserve this past weekend, Powell stated, “We do not seek or welcome further cooling in labor market conditions,” adding that “The time has come for policy to adjust.”

And the market expects he’ll deliver.

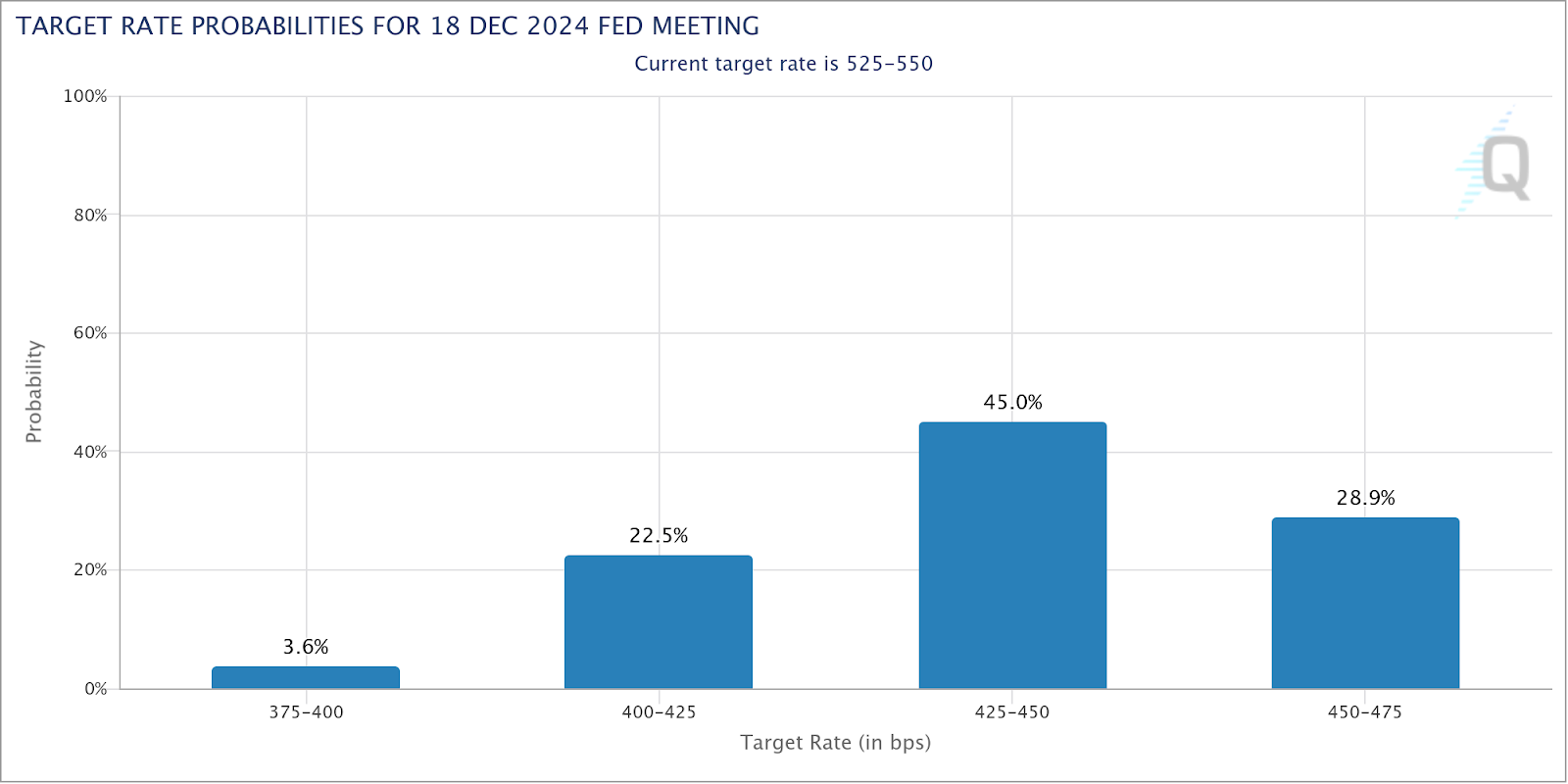

By year’s end, the odds on favorite is for 100 bps of cuts, with a 45% chance the Fed takes rates from its current 5.25% to 5.50% target down to 4.25% – 4.50%.

Source: CME Fedwatch

Together, the distribution of those odds adds up to a 96.4% likelihood of at least 75 basis points.

Despite the stock market’s near-record highs, near-record valuations, corporate sales growth, and still historically low levels of unemployment, somehow, the Federal Reserve feels that jobs need a boost.

You could call the willingness to cut now politically motivated. However, that contradicts assertions by the Fed of their rigorous independence.

And I would never challenge the official narrative.

But were I to question their timing, here’s what I would call out…

Jumping the Gun

The Fed usually gets spooked into cutting when the market turns down hard.

But with the S&P 500 within 2% of all-time highs, it’s hard to make the rate-cut case.

Source: ThinkorSwim

We’re also seeing stock market valuations that haven’t been this rich (e.g., they haven’t priced in this much earnings growth) since the market got over its internet bubble hangover more than 20 years ago.

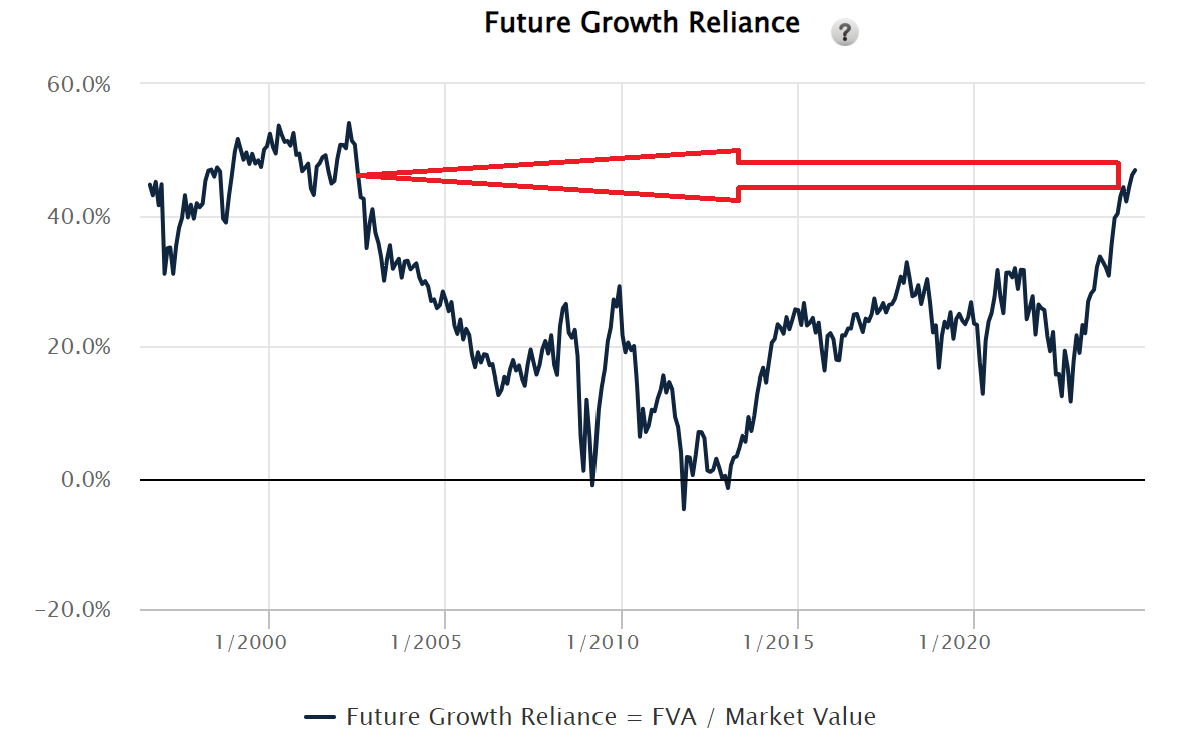

Source: ISS Investor Express

A Future Growth Reliance of over 46% means the S&P profits (as measured by economic value add) must grow at a sustained rate of nearly 2%, a feat they have only managed briefly on 3 occasions this century.

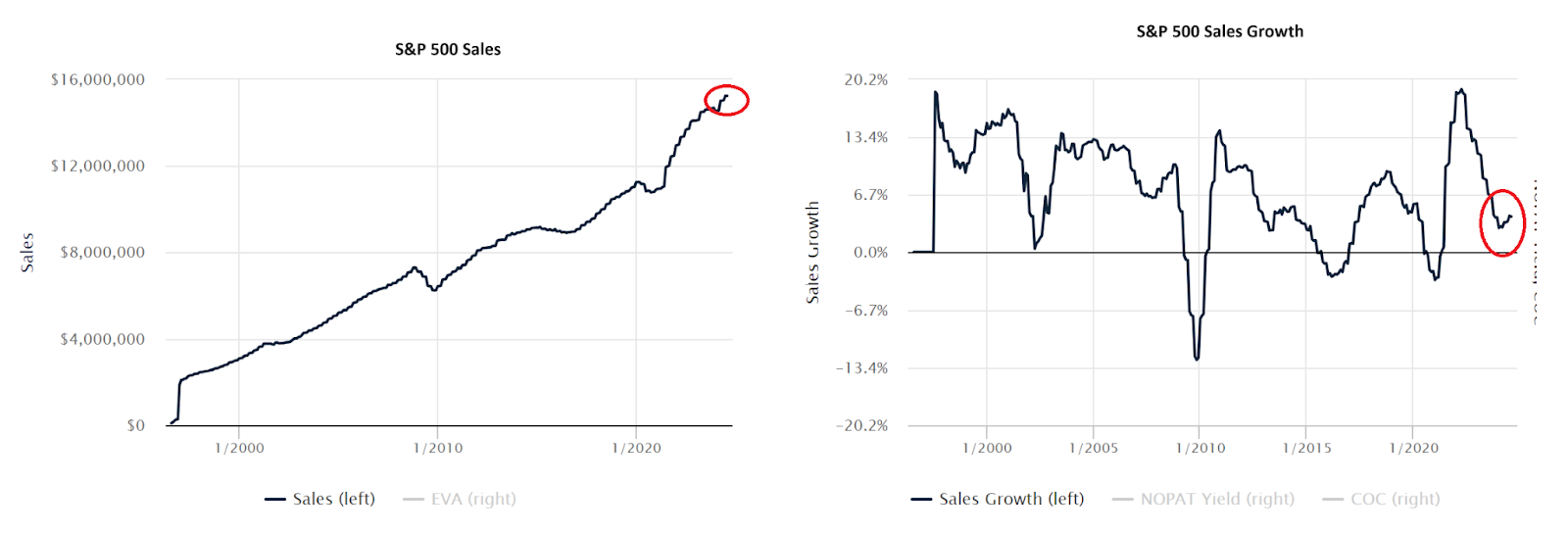

Sales among S&P 500 companies also remain positive. Moreover, sales growth has not declined, only cooled from historically high levels. The growth rate remains positive—in fact, it’s increased over the last few months.

Source: ISS Investor Express

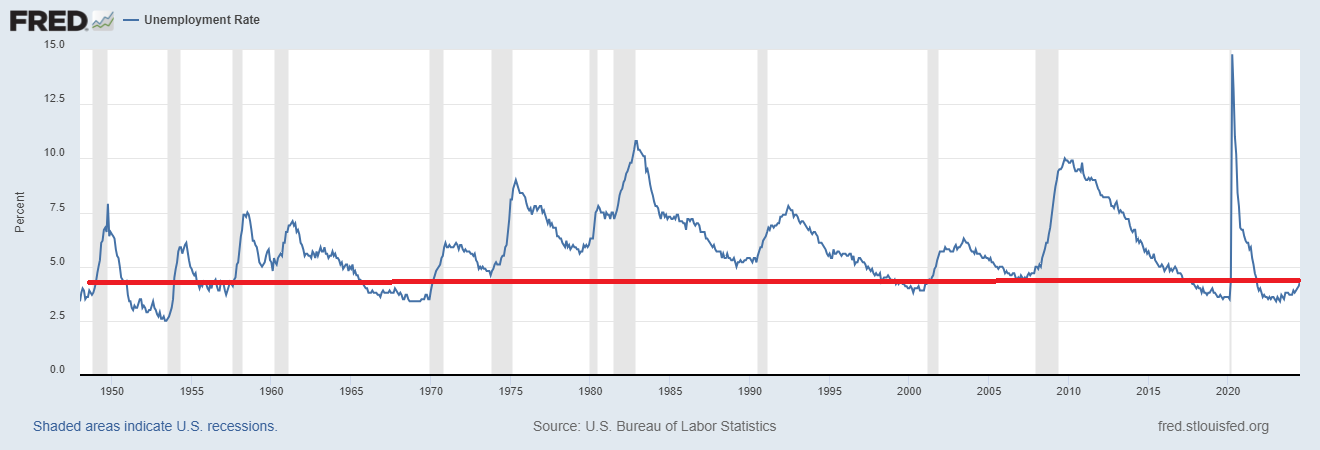

And the current 4.3% unemployment rate, though up a bit from its 3.4% low set last April, doesn’t figure as “weak” by any stretch of the imagination.

Perhaps the Fed sees China’s slow-burning economic collapse as a clear problem coming down the pike.

It could be that the BOJ’s fleeting flirtation with rate hikes uncovered some deep, structural issues that the Fed needs to nip in the bud.

They could also be preemptively heading off the collapsing commercial real estate sector, buying banks time and some breathing room to rework unpayable loans.

Or maybe, like any other entrenched D.C. political elite, they will do whatever they can to keep Trump out of the White House.

It’s hard to say why.

But no matter the reasoning, it’s clear the Fed wants to cut rates. And they will get what they want.

Brace yourself. The Fed could be lighting a fire under stocks while lighting a fire under inflation at the same time.

Editor’s Note: Want more Big Picture perspective? Join The Capital List here.

Think Free. Be Free.

Don Yocham, CFA

Managing Editor of The Capital List

Related ARTICLES:

Adjusting to the Fed’s New Reality

By dustin

Posted: November 15, 2024

There’s a new era for money emerging, and the Federal Reserve must adjust to the new reality. You saw some evidence of that this...

Flawed Motive Behind the Fed’s Rate Cut Agenda

By dustin

Posted: August 27, 2024

For every thing, there is a season. According to Jerome Powell, the season calls for cuts. At the annual Jackson Hole confab held by...

The Central Flaw of Central Bankers

By dustin

Posted: August 16, 2024

It looks like the market hopped back on the bullish path. At least for the time being. The Bank of Japan’s (BOJ) promise not...

The First Fiat to Fall

By dustin

Posted: August 7, 2024

Central bankers think they wield the Ring of Power over price. But price will not be denied. It will always have its way. The...

Always Look Cool

By dustin

Posted: August 5, 2024

A few years ago I did a military-type event called the “GoRuck Challenge.” It began at 7:30 PM, and for 13 hours I, along...

FREE Newsletters:

"*" indicates required fields