Nvidia: The Only Game in Town

Just a short update for you on Nvidia Corp. (NASDAQ: NVDA).

I’ll keep it high-level today and will have an updated Capital InFocus report for you next week.

I first laid out the opportunity to own this most essential AI company in September when the stock was trading around $108. My original Capital InFocus report walked you through the fundamentals that I felt put the $140 price for the stock easily within reach.

It has since surged past $150, though it gave up some of those gains over the last couple of days and is now trading at $136. With that tremendous run behind us and last week’s earnings release, it’s time to dive in again for an updated look at the company’s performance.

Profits doubled at what is once again the world’s most valuable company. Microsoft, Google, Meta, and xAI count among Nvidia’s customers. They are going all in on superclusters or server racks with 100,000 Blackwell chips (several times more powerful than previous chips).

And with a backlog of over 12-months, consensus estimates of $185 billion in revenue over the next year look well within reach.

Data Center Revenue more than doubled to a record $30.8 billion and now accounts for over 85% of total revenue.

Nvidia shipped 13,000 samples of its new Blackwell AI chip last quarter, which are now in full production. Reports of overheating caused some concern, but they have since been addressed.

Supply chain issues are the only real hurdle to Nvidia hitting revenue targets. But the 12-month backlog in orders shows that their Blackwell chips are the only game in town.

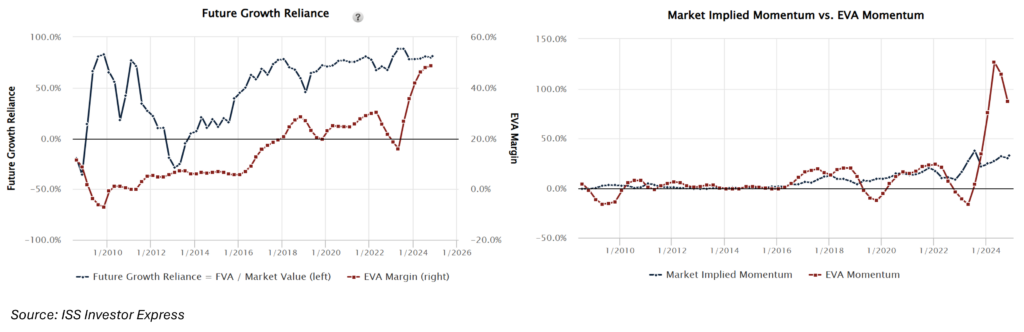

Despite the 25% rally from September, valuations based on Future Growth Reliance remain at 80%. Competitive profit margins (EVA Margins) increased to compensate for the higher price. And though the profit growth rate has slowed (EVA Momentum), they are still growing at a stunning 87% over the prior year.

Compare that 87% growth to the 32% growth rate required to justify the $136 price (Market Implied Momentum), and it’s clear Nvidia’s stock still has plenty of room to surprise on the upside.

I’ll have an updated Capital InFocus report ready for you in the next couple of days.

In the meantime, you can get up to speed on the long-term fundamentals of the company in this report.

You’ll hear from me soon.

Think Free. Be Free.

Don Yocham, CFA

Managing Editor of The Capital List

Related ARTICLES:

AI Eating Itself

By dustin

Posted: December 20, 2024

Nothing goes up in a straight line forever. Every trend, process, or dynamic has limits. They encounter negative feedback loops that send them running...

How To Keep This Market Moving

By dustin

Posted: December 11, 2024

The market keeps flying. The S&P hit a new all-time high of 6,099 yesterday. That’s up 28% for the year, and 75% from the...

Crushing the Competition

By dustin

Posted: December 3, 2024

Nvidia’s Blackwell AI processors continue to dominate the chip market. Two short years ago, Nvidia Corp’s (NASDAQ: NVDA) sales were growing in line with...

Nvidia: The Only Game in Town

By dustin

Posted: December 3, 2024

Just a short update for you on Nvidia Corp. (NASDAQ: NVDA). I’ll keep it high-level today and will have an updated Capital InFocus report...

The Pilgrims Guide to Voluntary Slavery

By dustin

Posted: November 27, 2024

It’s Thanksgiving time, which reminds me of America’s first collectivist experiment – the Pilgrims that landed at Plymouth Rock. Now, collectivism wasn’t necessarily the...

Who Pays for Trade

By dustin

Posted: November 8, 2024

“Consumption is the sole end and purpose of all production.” – Adam Smith With Trump on deck, American’s are scrambling to understand his favorite...

Capital Won the Election

By dustin

Posted: November 7, 2024

The uncertainty meter dropped dramatically yesterday. Trump’s overwhelming election victory gave markets some much-needed clarity. That clarity was still driving the S&P 500 to...

A New Game Just Like the Old Game

By dustin

Posted: October 20, 2024

For 80 years, the U.S. dollar has dominated world trade. That dominance began with the Bretton Woods System in 1944. Suffice it to say...

The Cost of the Dollar Status Quo

By dustin

Posted: October 15, 2024

Yield power over money to any sovereign power, and history proves they will abuse it. Expecting anything different makes as much sense as leaving...

Capital Components

By dustin

Posted: September 25, 2024

Here’s a breakdown of the components of a company’s capital base with an illustration of what that breakdown could look like for a company....

FREE Newsletters:

"*" indicates required fields