Coming Down the Mountain

Throughout the commercial computer era, which began roughly in 1970, Intel Corp. (NASDAQ: INTC) remained a leader among chip makers.

You could say it made private computing possible with the introduction of the Intel 4004 chip in 1971, the company’s first microprocessor.

I’ve personally never owned a PC without “Intel Inside.” The processing speed of their Core processors was the only chip that could handle my Excel models.

For decades, Intel set the standard for CPUs.

It stumbled with the rise of mobile phones – Qualcomm owned that segment. Nvidia has dominated graphics since 2000.

But when it came to delivering sheer computing power, other chip makers found Intel hard to beat.

At least until AI hit the scene in late 2022.

From June 2022 to June 2023, revenue dropped to $54 billion, down 26% from the $73 billion for the prior twelve months, accelerating a decline from its revenue peak of $79 billion in 2020.

Among the top twelve semiconductor stocks, its market share has fallen from the King of the Hill to third, with Nvidia now holding the crown. And the company still will not recover its revenue peak by the end of this decade, according to analyst estimates.

Jane’s Addiction “Mountain Song” comes to mind.

Look under the hood, however, and you’ll see that Intel isn’t just coming down the mountain. It has fallen flat on its face.

Less Than the Sum of Its Parts

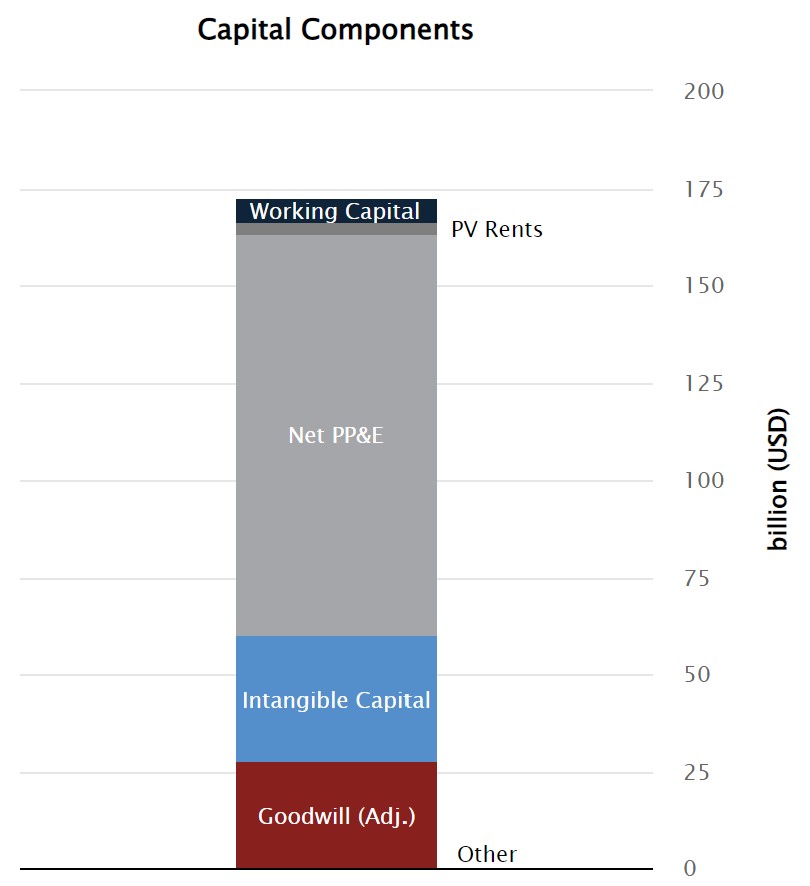

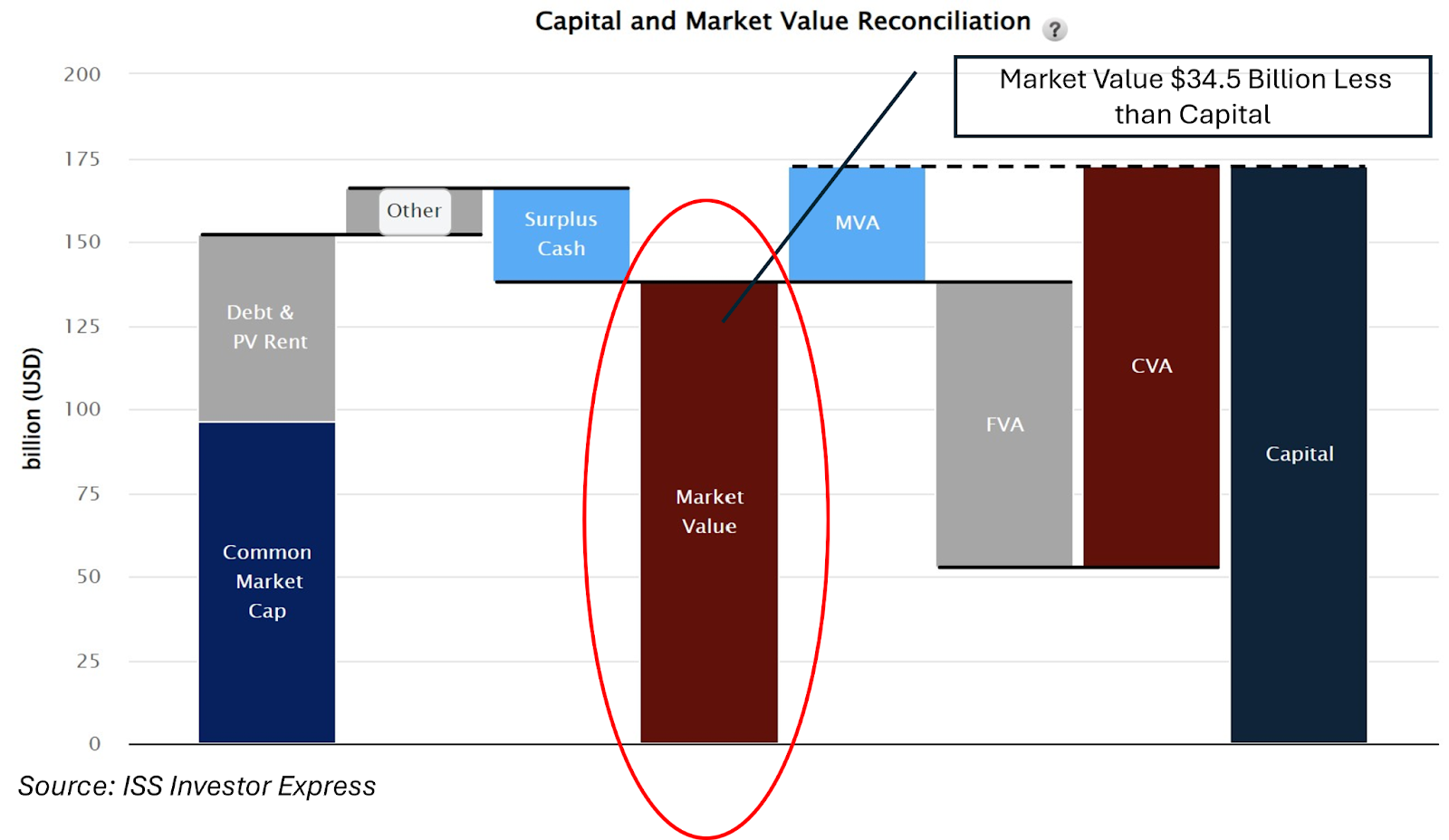

As of the most recent quarter, Intel had $172.4 billion in capital.

Source: ISS Investor Express

Compare the value of that capital base to Intel’s market value – the sum of its equity, debt, and surplus cash – and you’ll see that the market values Intel less its capital.

In other words, at $22.38 per share, it’s worth less than the sum of its parts.

The reason for that comes back to competitive profits.

In 2020, Intel generated over $12 billion in competitive profits, or 15% of its $79 billion peak revenue.

Those profits have since collapsed to a $11.6 billion loss – a near 200% swing to the downside.

Rolling the value of losses into the future (CVA above) amounts to over half of Intel’s capital base. With a meager 6% annual revenue growth expected over the next 5 years, Intel can’t grow itself out of the market value hole dug by its current loss rate.

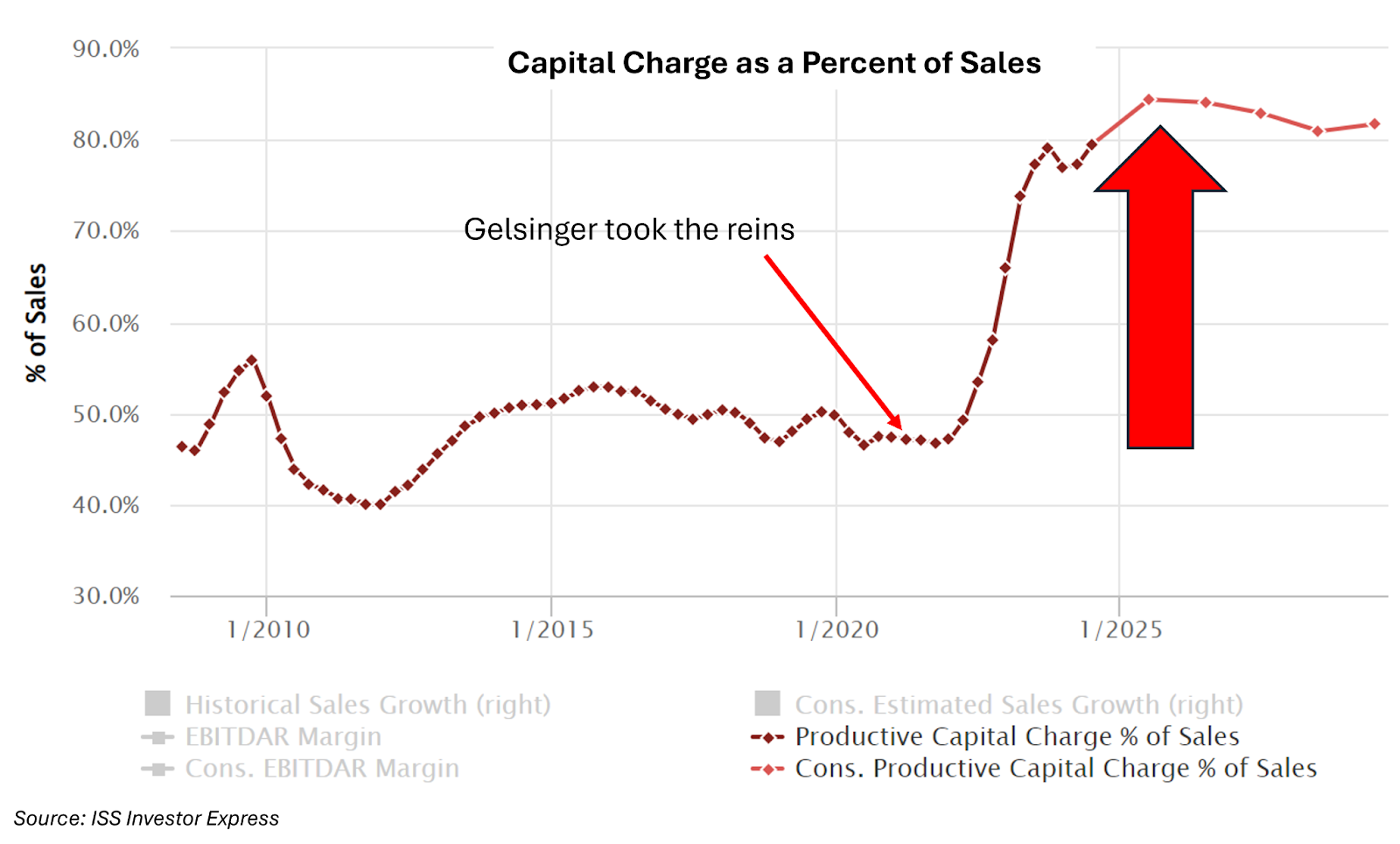

The man who dug that hole is Intel’s CEO, Pat Gelsinger, and his IDM 2.0 strategy.

Between a Rock and a Hard Capital Spot

IDM stands for Integrated Device Manufacturer.

It describes companies that design, manufacture, and sell their own semiconductor products rather than outsourcing the manufacturing. Intel’s IDM 2.0 strategy specifically aims to expand Intel’s capabilities by producing chips for other companies in addition to making its own, thus incorporating both integrated manufacturing and foundry services.

Note this is precisely the opposite of Nvidia’s (NASDAQ: NVDA) business model.

Nvidia outsources essentially all manufacturing to Taiwan Semiconductor and other manufacturers. Nvidia creates value through chip design innovation. It leaves chip manufacturing, a low-value commodity business, to others.

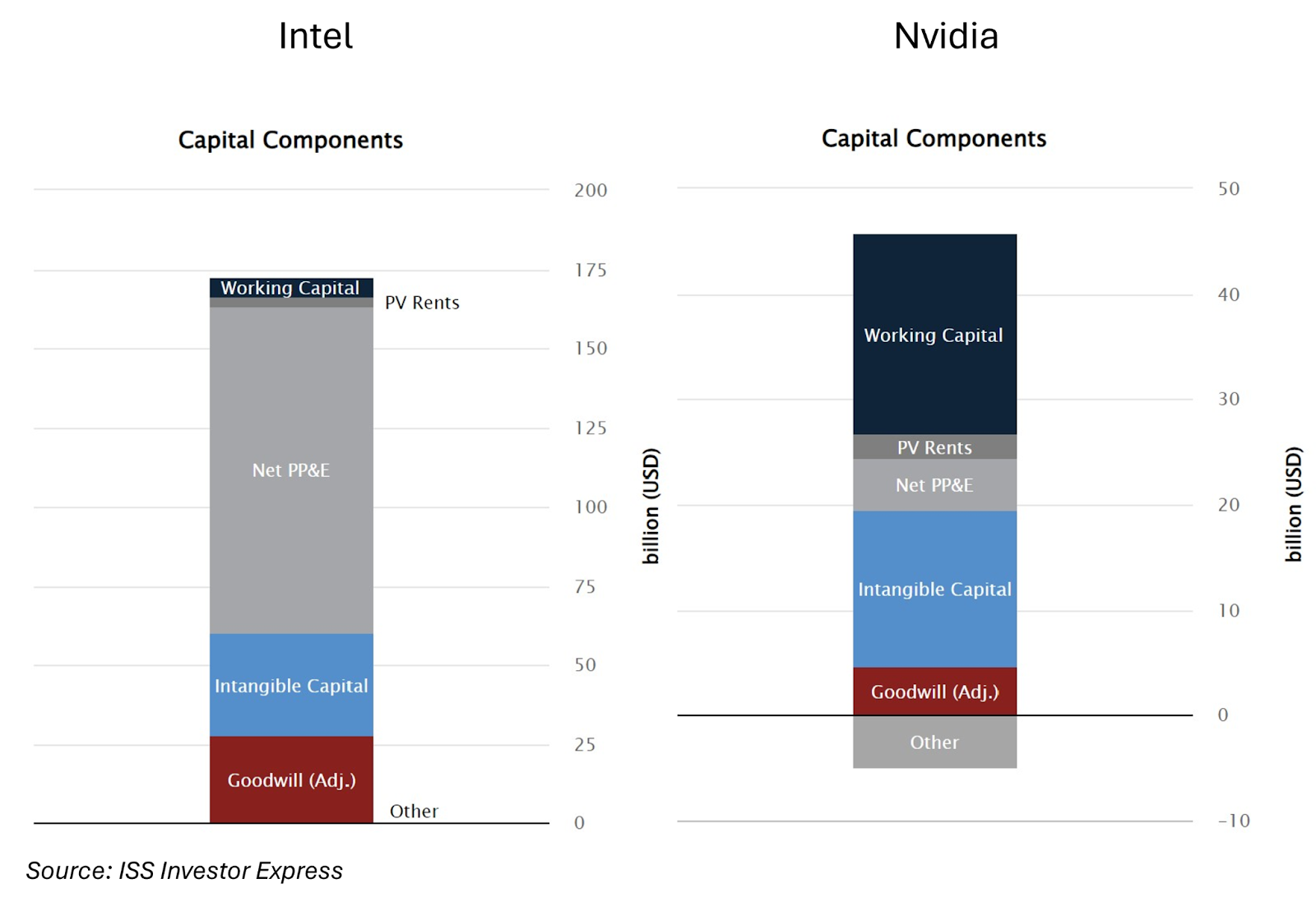

This outsourcing gives Nvidia a low capital-intensity business. To highlight that point, Intel carries $172.4 billion in capital, while Nvidia has only $41 billion.

Intel’s capital is 4 times the capital of Nvidia, but Nvidia generated $96 billion in revenue over the last year compared to Intel’s $54 billion – or nearly double the revenue with less than one-quarter of the capital.

And of that capital, Intel has tied up 60%, or $103.4 billion, in hard assets like property, plant, and equipment (net PP&E). Nvidia’s PPE is only 12% of total capital.

Rather than refocusing the company’s investments on Intel’s strength in innovation when he took over in February of 2021, Pat Gelsinger drove Intel into low-value commodity manufacturing.

Since early 2023, Intel has bet the farm on its foundry business with a significant focus on transforming its operations to serve external customers.

It was a disastrous move.

Operating losses began piling up in 2023, in part due to high development costs and an aggressive investment plan, which includes over $100 billion in new fab capacity globally.

That capital ain’t free. It comes with a steep cost, is mostly fixed, and hard to downsize. You can see the steep rise in the cost of that malinvestment below.

Those costs eat away at revenue that would otherwise flow into profits. Plus, those revenues have collapsed.

There’s not much to like about Intel’s prospects. Its losses and poorly performing fixed capital base make it a tough pill for potential buyers to swallow.

I’ll cover those details, including what value remains in Intel’s business, in my next Capital InFocus report.

I’ll have that report ready for you soon, so keep an eye on your inbox.

Until next time.

Think Free. Be Free.

Don Yocham, CFA

Managing Editor of The Capital List

Related ARTICLES:

American Exceptionalism, v2.0

By dustin

Posted: February 12, 2025

The years following WWII brought America into an era of exceptionalism. We emerged as the war’s only true victor. Fighting the war necessitated a...

The Holy Trinity of Growth

By dustin

Posted: February 7, 2025

The War for the American Way has begun. Since taking office on January 20, Trump and his administration have launched a full-scale assault against...

The War for the American Way

By dustin

Posted: February 7, 2025

Since his ascension to office on January 20, Trump and Co. have launched a full-scale assault on the vast, unaccountable bureaucracy draining the U.S....

Draining the Moat

By dustin

Posted: February 2, 2025

DeepSeek threw a monkey wrench into a powerful AI narrative last week. It challenged the story that developing AI models requires capital that only...

Deep-Sixed AI Dreams

By dustin

Posted: January 28, 2025

Let’s play Never Have I Ever. I’ll go first. Never have I ever seen a market narrative crushed so thoroughly over a weekend. Until...

From FUD to Oil and Gas Clarity

By dustin

Posted: January 25, 2025

For the past four years, traditional energy stocks received no love from investors. Green energy initiatives hamstrung oil and gas stocks with fear, uncertainty,...

Waking Up to the “Drill Baby, Drill” Dream

By dustin

Posted: January 22, 2025

I first pointed out the opportunity emerging in traditional energy companies in August. As the Magnificent Seven lit up the charts with AI potentiality,...

This Ain’t Your Mother’s Internet Bubble

By dustin

Posted: January 21, 2025

Just a short note for you today as we head into the long weekend. You hear a lot about how the AI bubble is...

Tariff Winners and Losers

By dustin

Posted: January 17, 2025

T-minus 4 days until the terror becomes real in D.C. Inauguration Day will be upon us, and the D.O.G.E. becomes manifest for the parasite...

The Odds Favor Growth

By dustin

Posted: January 14, 2025

Capital markets don’t hide their expectations for the future; they hold them out for all the world to see. Assuming you know where to...

FREE Newsletters:

"*" indicates required fields