Pump the Brakes: Hairpin Turn Ahead

Markets look toppy.

The momentum that took the S&P from 3,491 last October to 5,669 by mid-July has changed its tune.

Source: TOS

The late August bounce petered out once Labor Day passed.

Perhaps the “AI Forever” believers now want proof that massive spending leads to profits.

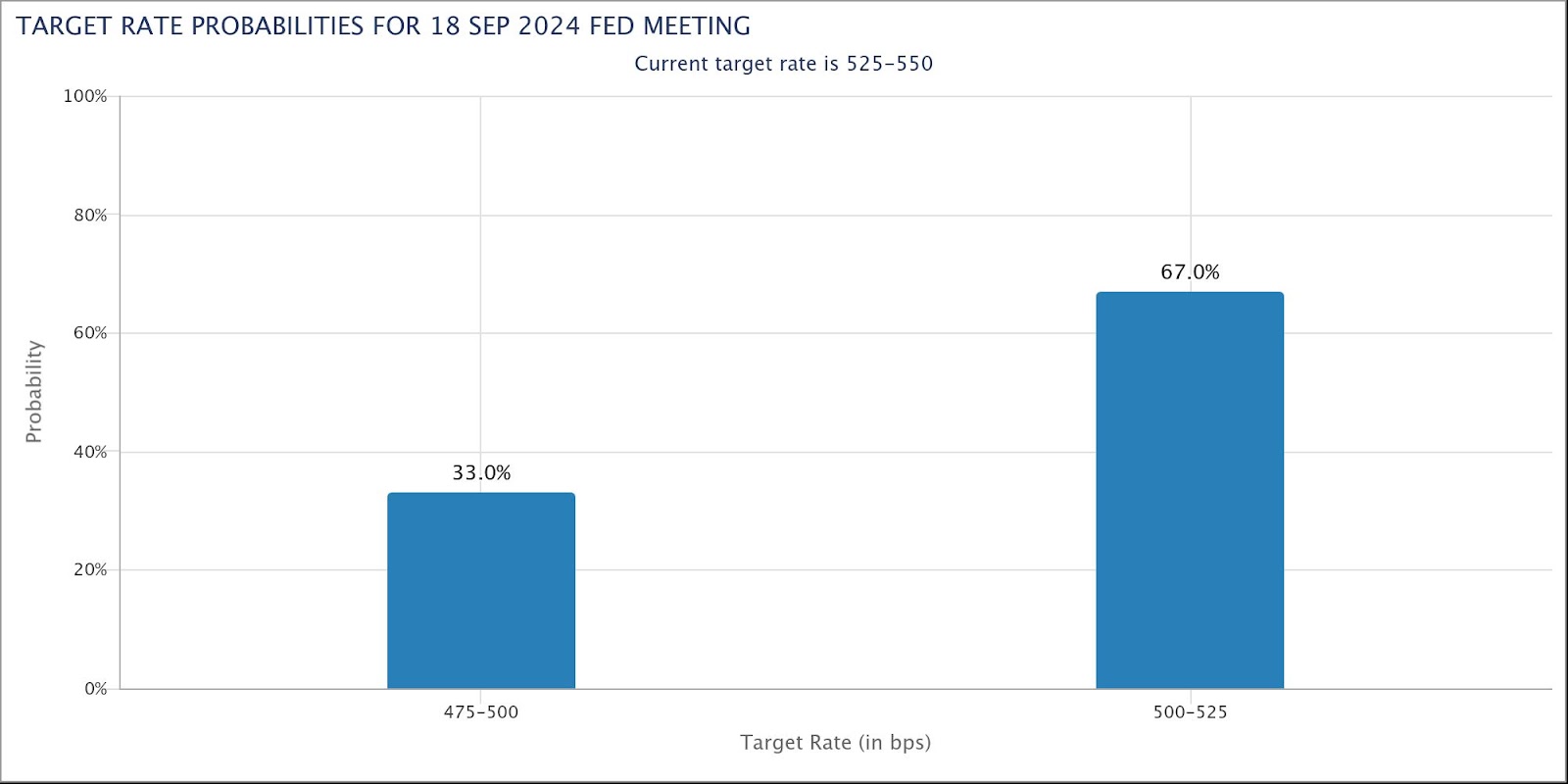

But don’t expect a Fed rate cut next week to bail stocks out.

Bond markets have fully priced in a 25 basis point cut, perhaps a little more, with Fed futures showing 67% and 33% odds of 25 and 50 bps cuts, respectively.

Source: CME FedWatch

So, a rate cut would be, at best, a push.

Now, they could signal significant cuts to follow. But that would panic markets more than anything else—and give Trump even more ammo to claim the Fed has political motives.

The Fed uses a slightly weaker job market to defend the rate cut posture.

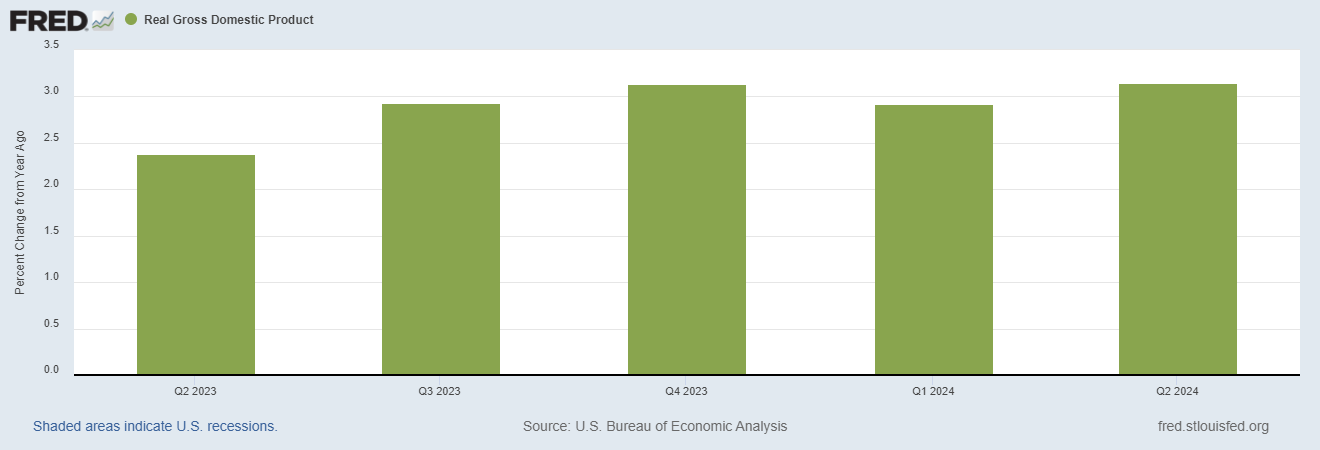

Though with the economy posting 3% growth for the last four quarters…

And with leading indicators pointing higher…

A rate cut seems hard to justify–at least when you look at the economic stats.

But look elsewhere, and you’ll see we’ve crossed the line that recession always follows.

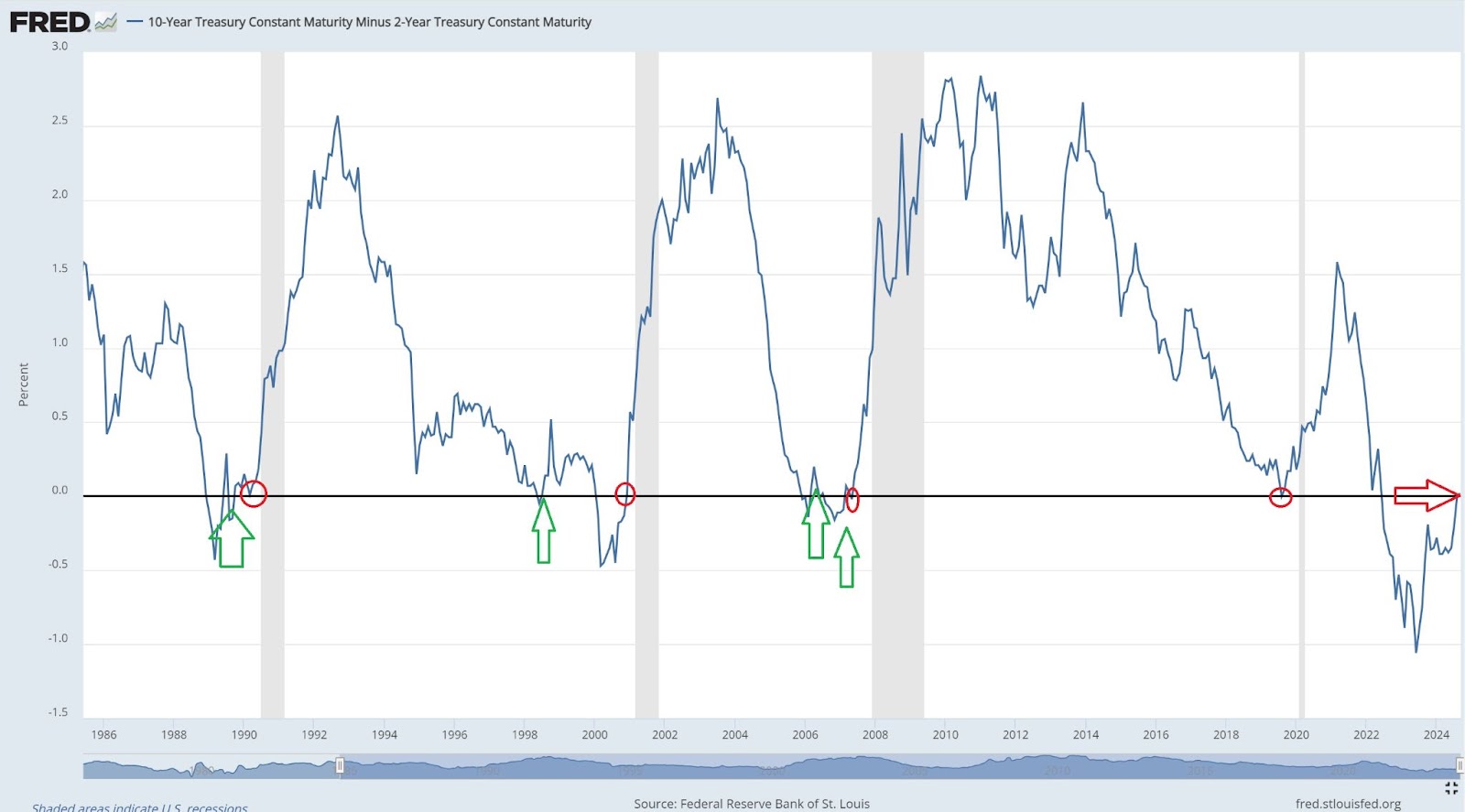

The Line that Leads to Recession

In a typical market environment, the longer a bond’s maturity, the higher the interest rate.

Extremely short maturities (money borrowed at the Fed Funds rate is overnight money) carry the lowest interest rate, 2-year bonds typically pay more, and bonds 10-year or longer pay the highest premium.

This upward-sloping yield curve reflects the time value of money (lend money longer, and you expect more compensation).

It’s not always like that, however.

When recession fears rise, investors who typically hold stocks cut their equity holdings and seek safety in bonds.

This additional buying bids up bond prices, lowering their yield. Investors accept lower yields because a guaranteed lower bond yield beats an expected negative stock return. 10-year bonds pay less than 2-year bonds because “return of capital” trumps “return on capital” when market confidence slips far enough.

Take that dynamic all the way, and the yield curve “inverts.”

The yield curve can also invert when the Fed forces short-term rates higher.

In this case, which is usually the case, rather than market players anticipating a recession and driving long-term rates lower, the Fed triggers a recession by pumping the brakes through rate hikes.

Eventually, the economy slows, and the Fed reverses course and cuts rates.

These cuts (or the expectation of cuts) revert the yield curve to its normal, upward-sloping state. And that’s when you know a recession is on its way.

The chart below shows this changing state since 1985, with official recessions shaded in grey.

The blue line above zero means 10-year yields are higher than 2-year yields–that’s normal.

Dropping below that line means yield-curve inversion.

The red circles point to every reversion to normal during that time. Each time it reverts, a recession soon follows.

The green arrows point to head fakes. Not that a recession didn’t follow, but the rate curve played back and forth with inversion and reversion before the official recession kicked in.

As the red arrow shows, we’ve now crossed the line beyond which recession always follows.

And, with one exception, markets never rally into recession.

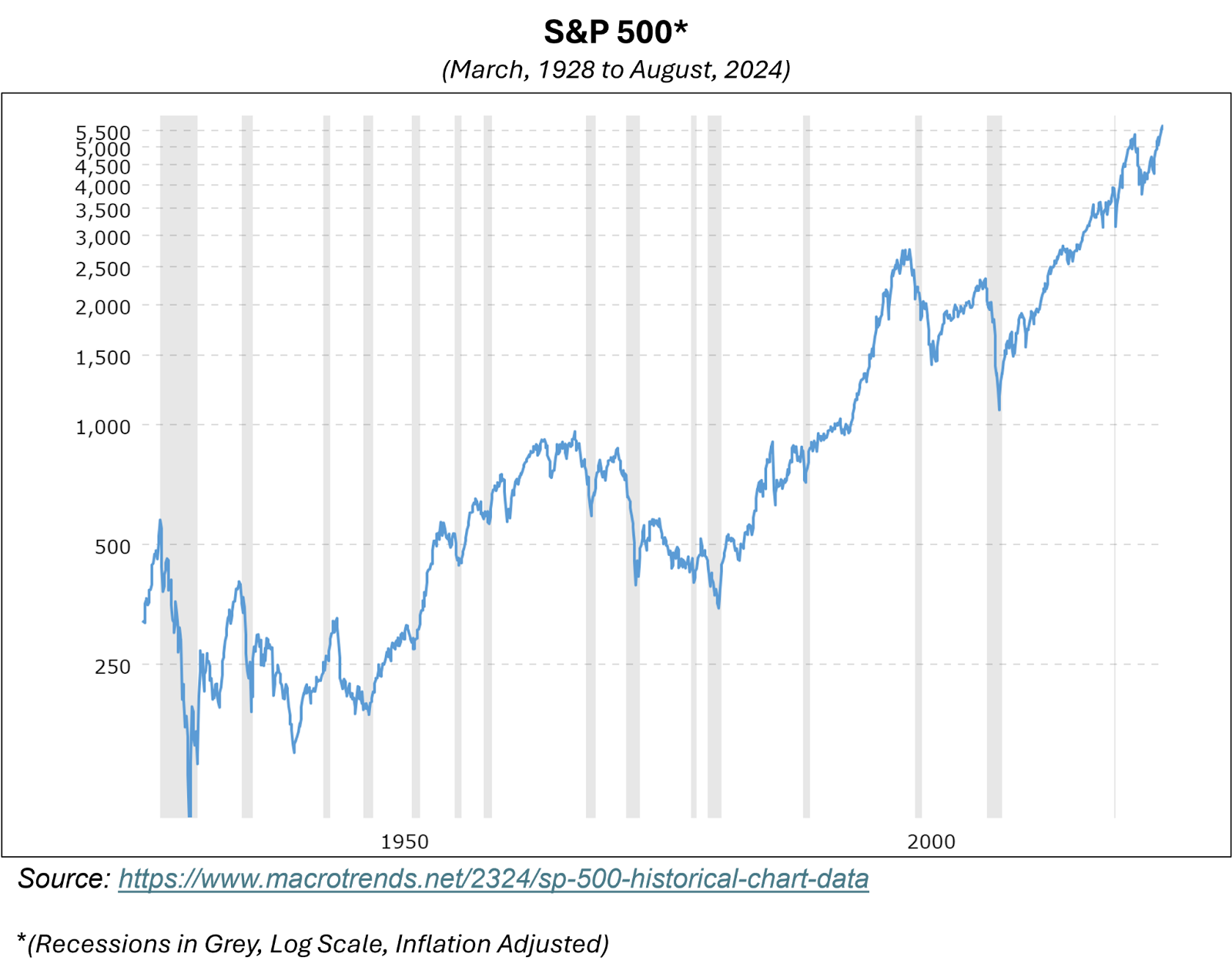

Wind It Way Back

The chart below shows the S&P 500 all the way back to 1928, with the 15 recessions that occurred during that time again shaded in grey.

With the exception of the end of WWII, markets always sold off by the time the economy entered recession.

Now, of course, the Fed is cutting because they hope to head off a recession.

That’s the mythical “soft landing” that you hear everyone talking about.

But they won’t head it off. That line has been crossed. And markets will sell-off before its all said and done.

Granted, a recession could take some time to play out, 20 months at the extreme, based on history.

And, like I said, the stats still point to growth.

But a recession is heading this way.

And now is not time to go all in on stocks thinking you can call the top.

Think Free. Be Free.

Don Yocham, CFAManaging Editor of The Capital List

Related ARTICLES:

AI Eating Itself

By dustin

Posted: December 20, 2024

Nothing goes up in a straight line forever. Every trend, process, or dynamic has limits. They encounter negative feedback loops that send them running...

How To Keep This Market Moving

By dustin

Posted: December 11, 2024

The market keeps flying. The S&P hit a new all-time high of 6,099 yesterday. That’s up 28% for the year, and 75% from the...

Crushing the Competition

By dustin

Posted: December 3, 2024

Nvidia’s Blackwell AI processors continue to dominate the chip market. Two short years ago, Nvidia Corp’s (NASDAQ: NVDA) sales were growing in line with...

Nvidia: The Only Game in Town

By dustin

Posted: December 3, 2024

Just a short update for you on Nvidia Corp. (NASDAQ: NVDA). I’ll keep it high-level today and will have an updated Capital InFocus report...

The Pilgrims Guide to Voluntary Slavery

By dustin

Posted: November 27, 2024

It’s Thanksgiving time, which reminds me of America’s first collectivist experiment – the Pilgrims that landed at Plymouth Rock. Now, collectivism wasn’t necessarily the...

Who Pays for Trade

By dustin

Posted: November 8, 2024

“Consumption is the sole end and purpose of all production.” – Adam Smith With Trump on deck, American’s are scrambling to understand his favorite...

Capital Won the Election

By dustin

Posted: November 7, 2024

The uncertainty meter dropped dramatically yesterday. Trump’s overwhelming election victory gave markets some much-needed clarity. That clarity was still driving the S&P 500 to...

A New Game Just Like the Old Game

By dustin

Posted: October 20, 2024

For 80 years, the U.S. dollar has dominated world trade. That dominance began with the Bretton Woods System in 1944. Suffice it to say...

The Cost of the Dollar Status Quo

By dustin

Posted: October 15, 2024

Yield power over money to any sovereign power, and history proves they will abuse it. Expecting anything different makes as much sense as leaving...

Capital Components

By dustin

Posted: September 25, 2024

Here’s a breakdown of the components of a company’s capital base with an illustration of what that breakdown could look like for a company....

FREE Newsletters:

"*" indicates required fields